This Halloween, prepare to see too many sexy costumes, too many guys in t-shirts with stupid sayings, a guy in a Green Lantern costume but will it be ironic? All I know is someone better figure out how to make Netflix a costume. Below are my picks for the best of the best.

>>Best Of LA: Where To Get Halloween Costumes

1. iPhones/Steve Jobs/Anything Apple

Okay, so these guys are wearing working iPhones. Bravo. For the rest of us, why not make a t-shirt with the iPhone face, dress up as genius Steve Jobs, don yourself with a bunch of plastic apples from Michael’s or just go as one big apple.

2. Princess Beatrice

Oh yes. There is a fantastic knockoff of the most ridiculous fascinator in the world.

3. Michael Jackson

Nobody can stop watching Conrad Murray’s trial. Pay homage to MJ’s memory with the officially licensed Michael Jackson Bad costume.

4. Charlie Sheen

You can buy official Charlie Sheen shirts here.

5. Toddlers & Tiaras

There are many costumes to choose from, the hooker outfit in Pretty Woman, sexy cowgirl… prom queen… The best part? Bad Halloween wigs, fake tans and horrible frosted makeup work wonderfully! Begin building your costume with this wig, please.

6. Bridesmaids

If you don’t feel like working that hard on your costume, head to the back of your closet or Goodwill for tacky bridesmaids dresses. You must do this with a bunch of friends.

7. Amy Winehouse

Man, I loved me some Winehouse. In fact, I went as her for Halloween three years ago. You can’t go wrong with Zombie Winehouse.

8. Book of Mormon.

Get out your black slacks, a crisp white button up shirt, black tie, hair gel and a bright smile. Add a backpack and a helmet and you’re golden.

9. Flashdance

I know Footloose is the latest film buzzing, but I’m a sucker for Flashdance.

10. Royal Couple

The wedding has barely passed, but it’s kind of already feeling passe. Make them zombies. Zombies are the answer to everything. Or wrap a bunch of gauze dyed with tea around you and make them mummies!

11. Katy Perry/Nicki Minaj

I had Katy on my list last year, but this year, you can buy this everywhere.

If you have the guts to wear this costume, work it.

This blue wig could easily become Nicki Minaj with neon spandex.12. Angry Birds

Everyone has the game on their phone. Everyone will attend a party with an Angry Birds character.

Someone please go as the slingshot.

Friday, October 28, 2011

What are You Going to Be? Top Halloween Costumes of 2011

Thursday, October 27, 2011

Several Signs Suggest a Real Estate Rebound - Walnut Creek Real Estate News

[1]The past few weeks have showcased numerous signals that the real estate market is on the rise. Recently, we have reported statistics pointing to an industry turnaround, including a 15 percent rise [2] in housing starts in September; a surge in builder confidence [3] in October, an increase in mortgage applications [4] and a slew of regional market [5] improvements across the country [6].

Wednesday, October 19, 2011

Foreclosure Starts Fall Again

The Foreclosure Report - September 2011

After Big Jump in August, Foreclosure Starts Fall AgainAfter a significant jump in foreclosure starts in August, driven primarily by Bank of America, foreclosure starts returned to levels in line with prior months, far below the numbers reached at the peak. California has seen a drop in activity of 56 percent since its peak, from 58,623 Notice of Default filings in March of 2009 to 25,778 today. Arizona shows a similar swing in Notice of Trustee Sale filings, from 14,722 in March of 2009 to 5,982 filings last month - a decrease of 59.4 percent. Washington shows the greatest decrease of all, with 71.5 percent less Notice of Trustee Sale filings today than at their peak in June of 2009.10/11/2011Foreclosure sales were mixed this month, with declines in Arizona, California and Nevada, while Oregon and Washington both showed increases. Despite the declines, the percentage purchased by third parties, typically investors, was at or near peak levels. In California, third parties made up a record 27.4 percent of all sales last month. In Arizona, that number was even higher at 38.3 percent, also a record. Nevada was just shy of their record, set in August at 29.1 percent. Sales to third parties was up Washington was up 15.6 percent, a record for this year. Oregon was the only state to to show a decrease, down from 15.5 percent in July to 6.0 percent today.

"While foreclosure activity returned to its normal course in September, we fully expect to see more volatility like we saw in August as banks continue to work through robo-signing and other issues", stated Sean O'Toole, Founder and CEO of ForeclosureRadar. "We continue to believe that foreclosure activity is driven by political whim and financial institution solvency than by what's best for housing markets and the economy."

Tuesday, October 11, 2011

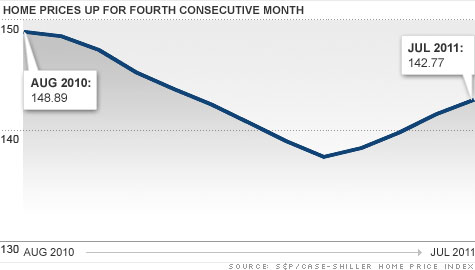

Home prices climb for fourth straight month - Sep. 27, 2011

Home prices climb for fourth straight month

September 27, 2011: 10:47 AM ETNEW YORK (CNNMoney) -- Home prices in July climbed for the fourth month in a row, but are still down from a year ago.

According to the latest S&P/Case-Shiller home price index of 120 major cities, prices rose 0.9% in July compared with June, but they're still 4.1% lower than 12 months ago.

"We are far from a sustained recovery" said S&P spokesman David Blitzer. "Continued increases in home prices through the end of the year . . . must materialize before we can confirm a housing market recovery,"

Adjusted for seasonal differences, the 20-city index was flat month-over-month.

But a handful of cities have shown surprising strength recently. In Detroit for example, prices jumped 3.8% month-over-month, after spiking 5.8% in June. Minneapolis prices increased 2.6% and Washington recorded a 2.4% rise.

Weakness continued in Las Vegas, which was down 0.2% month-over-month and in Phoenix, which edged 0.1% lower.

Blitzer cited some positive signs for the struggling housing market. Existing home sales were up 20% in August compared with 12 months earlier. Foreclosures have dropped most of the year.

On the negative side, however, housing starts are near historic lows and consumer confidence remains depressed.

"These combined statistics indicate the market is still bottoming and has not turned around," he said.

Stan Humphries, chief economist for the real estate website Zillow, is not optimistic about the outlook for housing.

"I still believe that the continued fears about a Greek default, weak employment growth and low consumer confidence will ultimately translate into weaker housing performance in the back half of this year," he said. "Looking ahead, expect fading monthly momentum in Case-Shiller."

Complicating things is that a quarter of homeowners are underwater on their mortgages, owing more than their homes are worth, making it difficult to refinance into low interest mortgages.

Underwater borrowers are also more likely to go into foreclosure since there's no home equity to tap should they run into a rough financial patch.

Even though most analysts can't work up much enthusiasm for the upward price trend, it's still welcome news, according to Anthony Sanders, a professor of real estate at George Mason University.

"Four months of price increases is a pretty good sign that the market has stabilized," he said.

A more stable market could mean that lenders will loosen up purse strings a bit, making it easier for potential homebuyers to get mortgages, which could pump up demand for homes.

That could happen, according to Sanders, but he expects some bad price trend news this fall as a weaker selling season begins.

Tuesday, October 4, 2011

How to Get a Home Loan With Bad Credit

How to Get a Home Loan With Bad Credit

--> By Sheree R. Curry| Posted Jun 29th 2010 5:52PM -->

-->

To easily snag a home loan, an applicant needs to be a "triple threat" -- have an excellent credit rating, a large down payment, and low debt-to-income ratio with steady significant income. But even if you have bad credit, you don't have to rule out future home ownership.

Homebuyers with bad credit due to a foreclosure or bankruptcy, or who have previously been turned down for a loan, can still get a home loan.

Melanye Miller, a 40-something Chicago schoolteacher, has been hankering for three years to move out of the single-family home she was renting, so that she could purchase a place big enough for her and her three children. But when her credit report revealed a poor score, she knew banks would not give her a home loan, especially not one with zero down payment.

To increase her chances of getting a home loan, Miller began a long road to recovery from her bad credit history, which included not using credit cards and setting aside money each month for her house fund. Finally, in November, after saving for almost two years, she purchased a four-bedroom condo. "I saved and saved, but I decided to purchase a foreclosure condo because it was less expensive and required fewer funds," she says. "Owning a home is not out of the question if you have bad credit. You just have to do your research, know what you can really afford, do even more research, and save your money."

There are hurdles, for sure. But for those with a less than stellar credit history, you need to highlight your "compensating factors" -- those mitigating factors not reflected in your bad credit score or on your credit report.

travel

Even though there are few opportunities for personal appeals when applying for a home loan -- for instance, explaining why a bill was not paid on time -- you can still try to present yourself in the best possible light. It just may help tip the scales in your favor when you've got bad credit in your history.

Here are seven compensating factors to consider submitting with your home loan application to help improve your chances for obtaining a mortgage, even with bad credit:1. Flaunt other assets. If you don't have a large cash reserve or a large down payment, show loan officers the financial assets you do have. For example, if you have whole life insurance, list the cash value on your home loan application. If you have a sizable 401(k) or other retirement accounts, be sure to list them all and their current values. This strategy lets lenders know that if you're ever in a bind paying your mortgage, you're able to pull from one of these other sources to make ends meet. And if you're seeking to refinance, showing a low loan-to-value rating is a huge plus.

2. Stress job stability. If you have been working in the same industry for several years, and even with the same company for, say, five years or longer, be sure to highlight that to offset a bad credit history. And don't forget to mention any regular pay raises that you've received. If you have a cost-of-living increase every two years, or an annual merit-pay increase, be sure to mention in your home loan application how your income has risen over the years. The same goes for regular bonuses. Proof of rising pay or additional money will help lenders know that you will have funds to offset any possible rise in expenditures, such as property taxes or utilities.

3. Show discipline. Prove to lenders that your bad credit is a thing of the past and that you know how to save. If you've been socking away $600 a month to a savings account or have been contributing yearly to a retirement account, this will help you obtain a home loan. You are trying to show discipline, consistency and stability.

4. Willingness to stay put. Prove to lenders that you're not a flight risk. Home loan lenders like to believe that you're going to stay put in that home for some time (though you can always upgrade or downsize). Show that you're committed to the home, neighborhood or greater community by listing how long you lived at your last residence, if the length of time was significant -- three years or more. If that time was spent living in your mother's basement, that might not fly, unless you show that the home you're interested in is down the street from Mom. Strong ties to the community can help.Essential How-To-Guides on AOL Real Estate: Home Buying, Selling, Renting, Moving and Home Improvement5. Increase your down payment. The days of zero down payments are pretty much gone. Yes, you can get a house with a 10 percent down payment, or 3.5 percent under FHA. But in general, the larger the down payment, the quicker the home loan approval. Historically, the single largest obstacle to purchasing a home has been amassing enough money for the down payment and closing costs. If you can't come up with that money on your own, there are a few down-payment assistance programs as well as state and local municipality programs to help. Check with your city for possible homebuyer assistance; show your banker that you're not afraid to ask for help and that you have the tenacity to solve any of your own financial problems.

6. Don't bite off more than you can chew. Be reasonable about the amount of house and home loan you can afford, even if some real estate agents or brokers are telling you that you can afford more. The best advice is to start out smaller than you want. Spend some time getting to know home prices in the area where you want to buy, and know that you always can move up later. It's far better to own a home you can afford than to move into something outside your payment comfort level -- only to lose it and amass more bad credit down the road.

7. Have proof. It's one thing to tell potential home loan lenders that you never were late on your rent, or that you always pay your child support obligations. It's another thing to be able to show them. Be prepared to give documentation to back up all of the items on your compensating factors list. For example, show canceled checks for payments you've made to any entity, show bank statements to prove regular deposits of income or contributions to retirement. A letter from a landlord saying that you paid rent on time is not enough. If you cannot produce these documents, you will raise doubts about the veracity of your credit history.

The bottom line is there are certain red flags that give home loan lenders pause. When your credit history is less than perfect, get past the warning signs by highlighting other, positive aspects of your financial profile.

Sheree R. Curry, an award-winning journalist, writes about personal finance and real estate. Her work has appeared in Fortune, the Wall Street Journal, theStreet.com, Entrepreneur, People and HousingWatch.com, among others.

Monday, October 3, 2011

Foreclosure Starts are Down Over 12% From Last Year - Real Estate News Walnut Creek

Data released by Lender Processing Services (LPS) Monday shows that foreclosure starts were up in August by 19.7 percent when compared to the previous month.

However, LPS noted in its report that the 247,957 foreclosures initiated in August represents a 12.2 percent decline from a year earlier.

At the same time, of the approximately 4 million loans that are either 90 or more days delinquent or in foreclosure, the number in the 90-plus day delinquency bucket – 2,148,179 – has contracted to levels not seen since 2008, according to LPS’ study.

That’s not the only indicator of improvement LPS documented for problem loans. The company’s latest report also showed that, of loans that were current six

months prior, 1.4 percent had become seriously delinquent by August.

LPS says that percentage is less than half the rate seen in 2009, when the loan deterioration rate peaked at 2.9 percent.